Table of Content

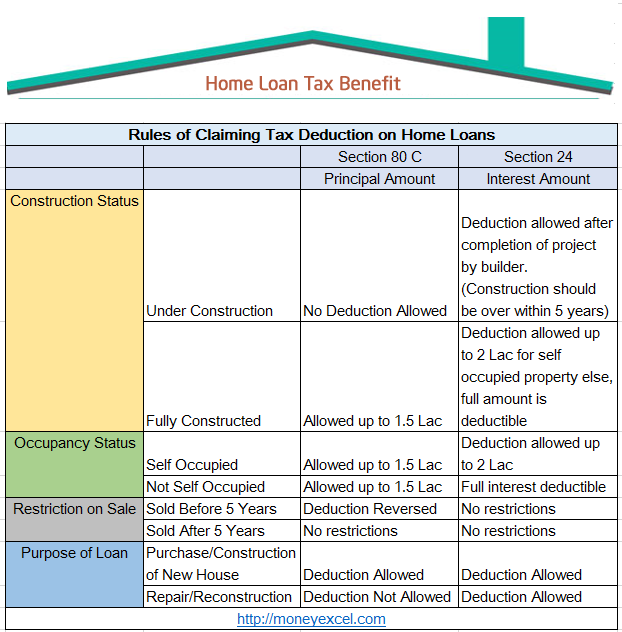

If a property is jointly owned, each co-borrower can claim Rs 1.50 lakhs as tax deduction on their respective incomes under Section 80C. For spouses to claim that benefit, they have to be co-owners, as well as co-borrowers. Deduction under Section 24 for interest paid can be claimed even if the money is borrowed financing institutions, or even friends or relatives. Deduction under Section 80C for principal repayment, cannot be claimed for money taken from friends or relatives. Any loss remaining unadjusted, can be carried forward and be set off against income from the same head, for eight subsequent years. IP PINs are six-digit numbers assigned to taxpayers to help prevent the misuse of their SSNs on fraudulent federal income tax returns.

The mortgage was a 7-year balloon note and the entire balance on the note was due in 1993. She refinanced the debt in 1993 with a new 30-year mortgage . On March 2, 2022, when the home had a fair market value of $1,700,000 and she owed $500,000 on the mortgage, Sharon took out a second mortgage for $200,000. She used $180,000 of the proceeds to make substantial improvements to her home and the remaining $20,000 to buy a car .

Tax Benefits on a Second Home Loan

Deductions under Section 80C are offered on the payment basis – deductions can only be claimed on the actual amount the borrower pays in a year. On purchase of property with home loans, borrowers enjoy a variety of deductions on their income tax liability. These deductions against the tax could be claimed under four sections of the income tax act, namely Section 80C, Section 24, Section 80EE and Section 80EEA.

Owing to the difficulties caused by the Coronavirus pandemic, there was a demand from sector stakeholders, to extend this time limit further, in order to incentivise buyers. Consequently, finance minister Nirmala Sitharaman extended the scope of this section for another year, i.e., till March 31, 2022, to provide an impetus to the sector. This is why there has been a long-standing demand that the deduction limit under Section 80C be increased, in order to justify the vast number of investment/expenditures it covers.

More Under Income Tax

The home can be a house, condominium, cooperative, mobile home, house trailer, boat, or similar property, as long as it has basic living accommodations (e.g., sleeping, cooking, and toilet facilities). Only first-time buyers can claim deductions under Section 80EE and Section 80EEA. This helps them make their combined deductions as high as Rs 5 lakhs per annum. The benefit will double, if the property is jointly owned. As per Section 24, a person can deduct amounts up to Rs 2 lakh an income tax rebate on home loan from their overall revenue for the interest element of an EMI you paid throughout the year. Planning to maintain a residence in your hometown, buying a holiday home, or planning to create a second income source by renting out your property; there can be many reasons to buy a second home.

If you pay off your home mortgage early, you may have to pay a penalty. You can deduct that penalty as home mortgage interest provided the penalty isn't for a specific service performed or cost incurred in connection with your mortgage loan. You may want to treat a debt as not secured by your home if the interest on that debt is fully deductible whether or not it qualifies as home mortgage interest.

Deductions under Section 80EEA

At all times during the year, at least 80% of the total square footage of the corporation's property is used or available for use by the tenant-stockholders for residential or residential-related use. A qualified home includes stock in a cooperative housing corporation owned by a tenant-stockholder. This applies only if the tenant-stockholder is entitled to live in the house or apartment because of owning stock in the cooperative. If you prepaid interest in 2022 that accrued in full by January 15, 2023, this prepaid interest may be included in box 1 of Form 1098. However, you can't deduct the prepaid amount for January 2023 in 2022. (See Prepaid interest, earlier.) You will have to figure the interest that accrued for 2023 and subtract it from the amount in box 1.

In addition, you can deduct any points paid by the seller. The buyer reduces the basis of the home by the amount of the seller-paid points and treats the points as if he or she had paid them. If all the tests under Deduction Allowed in Year Paid, earlier, are met, the buyer can deduct the points in the year paid. If any of those tests aren't met, the buyer deducts the points over the life of the loan.

But, before opting for second home, one should keep in mind the tax implications under the income tax act 1961 of the second home. If the home counts as a personal residence, you can generally deduct your mortgage interest on loans up to $750,000, as well as up to $10,000 in state and local taxes . If the home is considered an investment property , you can deduct expenses related to owning, maintaining, and operating the property.

It doesn’t matter how much rental income you earn in this period. In fact, you don’t have to claim rental income if you’re renting the property for 14 days or less. The limit on deductions is shared between up to two personal residences. A personal residence is any home you own that is not classified as an investment property. In case both your homes have been rented out, the rental income from these homes will be taxed. A total deduction will be available on the interest paid on thehome loanwhich will help you save a hefty amount.

This may allow you, if the limits in Part II apply, more of a deduction for interest on other debts that are deductible only as home mortgage interest. She sells the home for $100,000 to John, who takes it subject to the $40,000 mortgage. John pays $10,000 down and gives Beth a $90,000 note secured by a wraparound mortgage on the home. Beth doesn't record or otherwise perfect the $90,000 mortgage under the state law that applies.

This can be claimed in five equal instalments from the year in which construction is completed. This deduction is available with other eligible items like provident fund contribution details of which you can check on UAN member portal, life insurance premium, tuition fees, PPF contribution , NSC, ELSS, etc. This deduction is also available for any amount paid for registration and stamp duty of a residential house. The income tax laws do not have any restriction on the number of houses for which you can claim this deduction. The income tax laws also do not distinguish between self-occupied property or a let out property, for this purpose. So, although, you can take home loans for more than one property, the aggregate amount of deduction shall be restricted to Rs 1.5 lakhs, for repayment of the principal amount of all the home loans taken together.

You will have to key in details such as loan amount, loan tenure, interest rate, annual income, etc., while using the online calculator. If the home loan is taken out jointly, individual loan holders may deduct housing loan interest up to a total of Rs. 2 L from their taxable income, as well as principal payments per Section 80C until a total of Rs. 1.5 L. In case you forget to follow step 3, you will have to file income tax returns to claim the tax benefits.

No comments:

Post a Comment